Non-resident E-Commerce operator’s taxation in India- Basic understanding

Background: We all are aware that the operations through E- commerce operators have been tremendously increasing all over the world. Virtual market and shopping is a new trend everywhere. People are much interested in shopping through online as it provides many new features and options. Due to Covid-19 pandemic situation all over the world, operations through E-commerce will be increased manifold. Also, it is a fact that the tax laws around the word could not catch the pace with which the E-commerce operations have spread.

Before the setup of G-20 countries committee in order to tackle base erosion and profit shifting (BEPS), the tax laws of many countries (also bilateral treatise) provided to tax the business income of E-commerce operator only if such E-commerce operator has a permanent establishment in that country. In other words, the income of the non-resident E-commerce operator could be charged to tax in that country if some kind of activities is carried out in that country in relation to the business of the E-commerce operator. This is popularly known as territorial nexus of the operations of the non-resident E-commerce operator in that country.

Thanks to the internet facility which has made the whole world as one market. Due to technological advancement and internet facility, no operations or physical presence of such E-commerce operators is required in any country in order to carry business in that country. Consequently, the countries were facing difficulties to tax profits of such E-commerce operators due to lack of any physical presence or activities in such country. Precisely, this is the reason where BEPS action plan 1 specifies few measures which could be adopted by the member countries in order to tax the profits of non-resident E-commerce operators.

One of the options is to adopt equalization levy (EL) in the domestic law. India has recently adopted this equalization levy in the domestic law in Finance Act, 2020 by amending the Finance Act, 2016. The equalization levy is brought in the statue to specifically tax the profits of the E-commerce operators carrying business in India. This equalization levy would not be applicable for the online advertisement provided by the non-resident as separate equalization levy (in the form of withholding tax) is already operating in the domestic law.

Understanding of law

Indian tax law defines E-commerce operator as a non-resident who owns, operates or manages digital or electronic facility or platform for online sale of goods or online provision of services or both.

E-commerce participant is defined in the law as a person resident in India selling goods or providing services or both, including digital products, through digital or electronic facility or platform for electronic commerce.

E-commerce supply or services means the following:

- Online sale of goods owned by the e-commerce operator or

- Online provision of services provided by the e-commerce operator or

- Online sale of goods or provision of services or both, facilitated by the e-commerce operator or

- Any combination of activities listed above

It is proposed in the Budget 2021 to clarify that any one of the following activities performed online, would constitute “online sale of goods” and/or “online provision of services”:

- acceptance of offer for sale; or

- placing of purchase order; or

- acceptance of the purchase order; or

- payment of consideration; or

- supply of goods or provision of services, partly or wholly

It is also proposed to clarify that base amount on which EL to be levied is the gross consideration for E-commerce supply of goods or services. This is irrespective of the fact that such goods are owned/facilitated or services provided/facilitated by E-commerce operator.

Further, above referred E-commerce supply or services has to be made or provided or facilitated to the following persons:

- To a person resident in India or

- To a non-resident in the specified circumstances (target advertisement and sale of data)

- To a person who buys such goods or services or both using internet protocol address located in India

This EL would not be levied if the E-commerce operator has PE in India and E-commerce supply or services are effectively connected to such PE. It is also proposed in the Budget 2021 to provide that EL would also not be applicable if the transaction is charged to Royalty/FTS as per the domestic law read with DTAA.

With this background, different scenarios are discussed below for better understanding of the taxation of E-commerce operator. In all the scenarios below, it is assumed that the E-commerce operator does not have a permanent establishment in India and its turnover exceeds INR 20 Million in the relevant year.

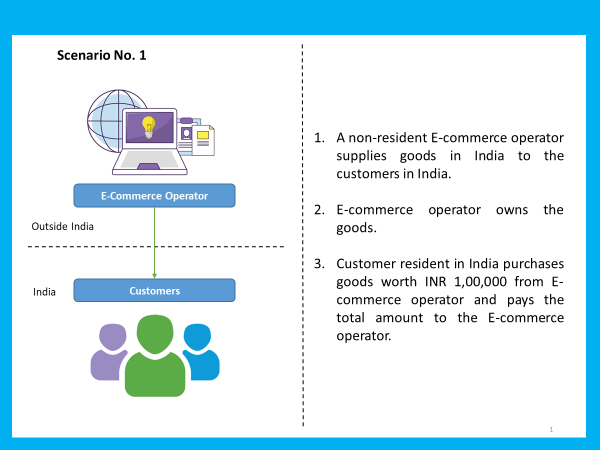

In this Scenario, it is very apparent that the E-commerce operator would be liable to pay equalization levy at 2% to the Indian Government. Reason being, all the following conditions laid down in the law is fulfilled:

- E-Commerce operator is a non-resident in India;

- Supply of goods is made to a person resident in India;

- The transaction is online sale of goods owned by the E-commerce operator

It may be noted that the equalization levy of 2% has to be applied on the total consideration of INR 1,00,000 received by the E-commerce operator as the law specifies levy has to be on the “consideration received or receivable“.

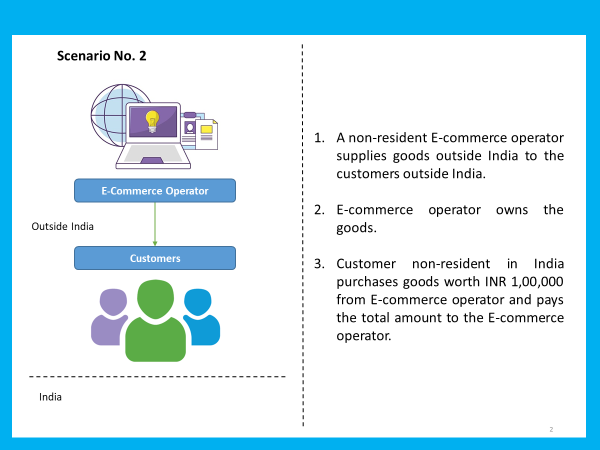

In this Scenario, it is very apparent that the E-commerce operator would not be liable to pay equalization levy as one of the conditions that the supply of goods has to be made to the person resident in India, is not satisfied. In this scenario, it may be observed that there is not even a virtual presence/tax presence of the E-commerce operator in India.

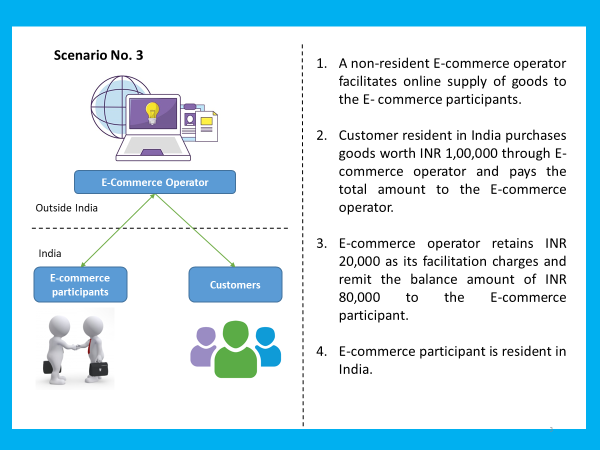

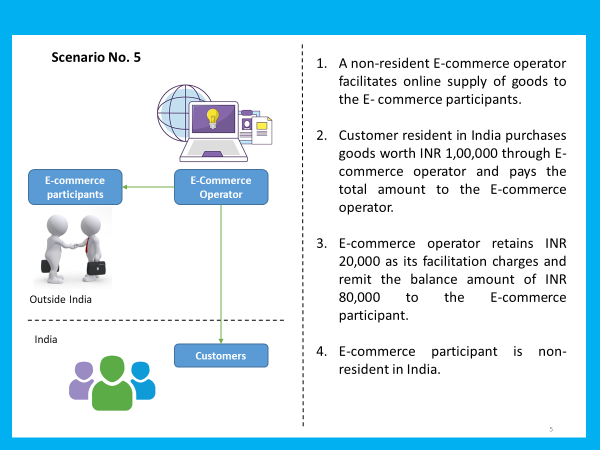

In this scenario, it may be noted that the E-commerce operator is providing only platform/facility to the E-commerce participant to supply goods to the customers. In other words, E-commerce operator is not the owner of the goods in this case. Generally, the privity of contract in these transactions is between the E-commerce operator and the E-commerce participant as the facility is provided to the E-commerce participant. As per the provisions of the Indian Income-tax law, in these cases, non-resident E-commerce operator would be required to pay Equalization Levy if the service recipient is resident in India. As the E-commerce participant is the service recipient and also resident in the above scenario, Equalization levy would apply.

A question may arise regarding the amount on which the equalization levy is required to be paid. Whether it should be INR 1,00,000 or INR 20,000? It may be noted that the consideration receivable by the E-commerce operator for providing the facility is INR 20,000. This is the gross amount of income in the hands of the E-commerce operator. Accordingly, the logical view would be to pay Equalization levy on the amount of INR 20,000. Interpretation of Equalization levy on INR 1,00,000 would result into absurdity as INR 80,000 is not at all the part of the turnover of the E-commerce operator. It is not accrued or arise or could not be construed to be earned by the E-commerce operator. Levying any tax on such amount which is not accrued in the hands of a taxpayer would be against the principles of law.

The above situation is now proposed to be clarified through Budget 2021 stating that EL has to be levied on total consideration of INR 1,00,000. Reason being, EL is not a tax on income but a separate levy on the concerned transactions.

Further, the domestic law provides that at the time of credit or remittance (whichever is earlier) of INR 80,000 to the E-commerce participant, the E-commerce operator would be required to withhold tax at 1% on such INR 80,000. Law also provides that in case the total consideration (INR 1,00,000) is paid by the customer directly to the E-commerce participant, still the consideration would be deemed to be paid to the E-commerce operator and the operator would be liable to withhold tax on INR 80,000.

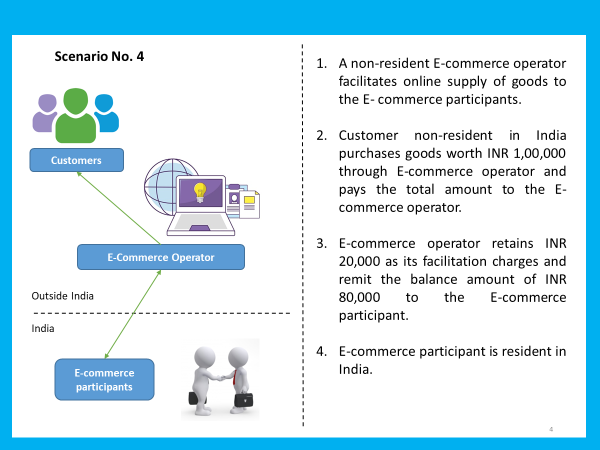

In this scenario, all the facts are similar as in the Scenario 3 except that the customer is a non-resident in India. In this case, the view as mentioned in scenario 3 would remain the same as it does not matter whether the customer is resident or non-resident in India. Reason being, the privity of contract is between the E-commerce operator and E-commerce participant. In other words, E-commerce operator is providing platform to the E-commerce participant. Residential status of the E-commerce participant is of importance as he is the person who is the recipient of facility from the E-commerce operator. As the E-commerce participant is resident is India, the E-commerce operator would be required to pay the Equalization levy.

However, in certain business models of the E-commerce operator, they may have an arrangement with the customer also and may charge consideration from the customer. In such a scenario, the residential status of the customer would also be relevant to analyse if the E-commerce operator is required to pay Equalization levy on such charges. If the customer is resident in India, the liability would arise in the hands of the E-commerce operator.

Withholding tax would apply to the E-commerce operator similarly as discussed in scenario 3.

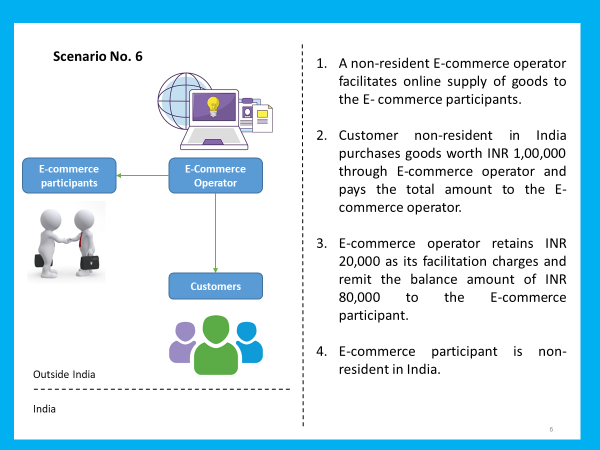

In this scenario, all the facts are similar as in the Scenario 3 except that the E-commerce participant is a non-resident in India. As the E-commerce participant is the service recipient from the E-commerce operator, its residential status is required to be checked. Therefore, in the above scenario, E-commerce operator would not be liable to Equalization levy as the E-commerce participant is non-resident in India.

However, please note that there are specific services (target advertisement and sale of data) on which E-commerce operator would be required to pay Equalization levy even if the service recipient is non-resident. These circumstance are not dealt in this post as the objective is to understand the basics.

Under this scenario, a very important question may arise that though the E-commerce operator has a huge customer base (who are resident in India), still it is not taxable in India only due to the reason that E-commerce participant is non-resident in India. It may be noted that the main objective of the BEPS action plan 1 is to recommend the ways in which the jurisdictions could collect tax from the E-commerce operators though they do not have a physical presence in the country but have a huge customer/user base in that country. Does it mean that the Indian legislation has made a mistake in not considering this scenario while drafting the law? The answer is No!!

Under this scenario, the concept of “significant economic presence” would come into picture. As per the Indian law, an entity may be having a significant economic presence in India if the customer/user base crosses a particular threshold or the total payments from India for the transactions carried out in India crosses a particular threshold in a year. Therefore, in case the E-commerce operator engages in systematic and continuous soliciting of business or interaction with users in India, then, it may create a permanent establishment for such E-commerce operator in India and a portion of its profits would be attributable in India as per the provisions of the law and treaty. Now it is critical to follow the fate of proposed Pillar 1 and Pillar 2 by OECD which would have direct impact on the aligning the provisions of “significant economic presence” in India.

In this scenario, it is ostensible that no Equalization levy would be applicable in the hands of the E-commerce operator as both the customer and the E-commerce operator are non-residents in India.

Note: Though the scenarios above only deals with supply of goods, all the above discussion would equally hold good for the supply of services by E-commerce operators or facility provided by E-commerce operator for supply of services.